Los Angeles wildfires expose a widening insurance gap — and why Australian premiums may rise

A catastrophe with global implications

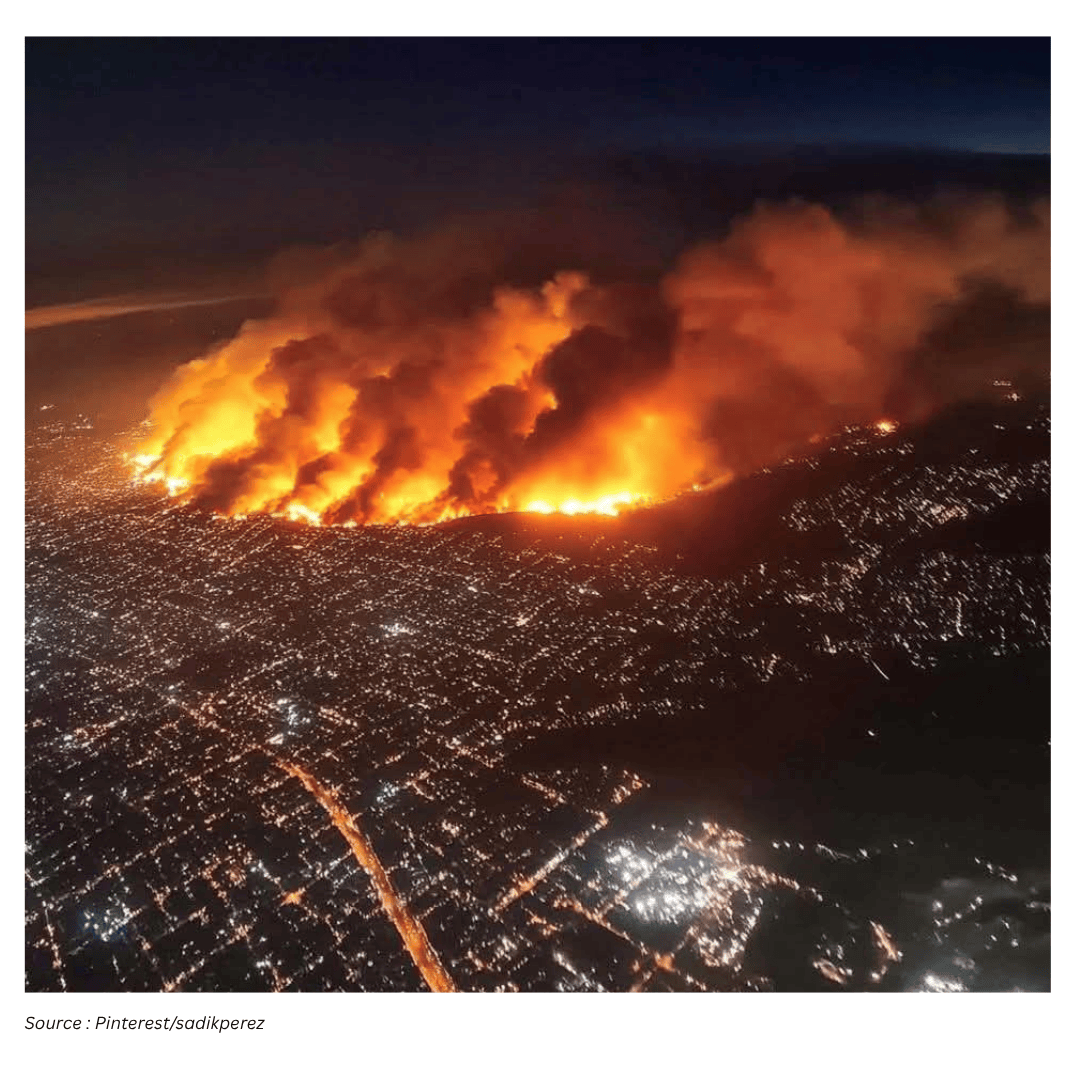

A series of wildfires in Los Angeles County has caused widespread devastation in California. The fires have resulted in at least 24 deaths, destroyed more than 12,000 homes and structures, and forced thousands of residents to evacuate. Authorities have warned the danger is not yet over.

Beyond the immediate human and physical toll, the event has also become a major stress test for insurance systems. Some estimates have put the cost of damage and broader economic loss at between A$400 billion and A$450 billion. Of that, only A$32 billion is insured. This disparity illustrates a central challenge in disaster recovery: large portions of losses can sit outside the insurance system, leaving households and governments to carry the financial burden.

Understanding the “insurance protection gap”

The difference between insured and uninsured losses is often described as the insurance protection gap. The Los Angeles fires provide a stark example of how wide that gap can become when catastrophic events hit areas with high property values and escalating risk.

As California rebuilds, uninsured losses will fall on property owners themselves and on public funds. This is not only a local problem. Large-scale disasters can reshape how insurers and reinsurers price risk, and those pricing changes can ripple across borders.

The protection gap has been growing in California as the state experiences increasingly devastating wildfires year after year. The trend matters because it shows how quickly an insurance market can shift from broadly available coverage to a patchwork of restricted options, higher premiums, and greater reliance on last-resort schemes.

Why insurers are pulling back in California

In response to growing risk, escalating insurance claims, and rising reinsurance and construction costs, at least a dozen of the largest property insurers have withdrawn from offering wildfire coverage in California or have restricted new policies. These insurers make up about 80% of the Californian market.

In March 2024, State Farm, the United States’ largest property insurer, announced it would not renew about 72,000 policies in selected California postcodes deemed too risky to insure for wildfire. Those postcodes included 1,626 homes in Pacific Palisades, the scene of one of the most damaging recent fires.

For insurers, the calculation is increasingly straightforward: it is becoming too expensive to do business in parts of California. When premiums no longer adequately cover expected claims and the cost of capital needed to support those risks, insurers either raise prices sharply, narrow coverage, or exit the market.

The rise of “last resort” coverage — and its limits

As mainstream insurers retreat, demand rises for alternative protection options. One such option is the California FAIR Plan, a state-legislated collaboration between insurers designed to provide wildfire policies for those who have been refused coverage elsewhere.

However, the FAIR Plan is deliberately “bare-bones”. Homeowners seeking cover for additional structures, theft and liability, or other perils may need to buy an additional top-up policy. Residential payouts are capped at US$3 million (A$4.8 million), which can leave many people underinsured.

Demand for the California FAIR Plan has surged since 2019, increasing by 164%. The combination of heightened demand and the scale of recent losses has raised concerns that the wildfires may bankrupt California’s insurer of last resort. The situation illustrates a broader dilemma: when private markets pull back, public or quasi-public schemes can come under pressure precisely when they are needed most.

Why Australians are paying attention

Australia is not immune to insurance affordability pressures, even without a disaster on the scale of Los Angeles occurring locally. The insurance protection gap is not unique to California, and some 15% of Australian households already face extreme insurance stress — defined as a situation in which it costs four weeks or more of pretax income to buy an insurance policy.

The Los Angeles fires are relevant to Australian policyholders for two reasons. First, they show how quickly wildfire risk can become an urban problem, not just a rural one. Second, they demonstrate how large losses can flow through global financial mechanisms that support insurance, potentially affecting premiums far from where the disaster occurred.

How a US wildfire can influence Australian premiums

Premiums in Australia may rise after the Los Angeles wildfires because insurance is not only a local business; it is also supported by a global reinsurance market.

To cover large-scale losses — such as those experienced during the 2022 floods in Australia — insurers typically buy reinsurance in the global market. In practical terms, insurers take out their own large insurance policies so they can pay out mass claims after major disasters.

The cost of global reinsurance capital can rise around the world as risk increases, losses mount, and reconstruction becomes more expensive. Reinsurance payments for wildfire losses in California therefore have the potential to create ripple effects in other insurance markets, including Australia. When reinsurance becomes more expensive, those costs can be passed through to consumers via higher premiums.

Local uncertainty adds to the pressure

The global reinsurance market is not the only factor that can push Australian premiums higher. There is also Australia’s own climate uncertainty and increasing risk of disaster.

Future extreme weather and the losses it may cause are becoming harder to predict. Where uncertainty rises, so do premiums, as insurers and reinsurers increase their capital reserving for potential losses. In other words, when the range of plausible outcomes widens, the financial buffer required to remain solvent also grows — and that can translate into higher prices for policyholders.

Wildfire risk is not confined to the bush — or to summer

One of the most sobering lessons from California’s crisis is that wildfires are not only a problem in rural areas or on the fringes of cities. The Los Angeles fires underscore that catastrophic losses can occur in densely populated areas and can even occur in winter, not just during a defined “wildfire season”.

Australia may have avoided a catastrophic citywide fire so far. But the intensification of bushfire seasons could ultimately create a similar insurance crisis here, especially if urban areas face direct exposure to fast-moving fires and widespread property loss.

Australia’s warning signs

Australia has had its own sobering warnings about the potential for suburban and peri-urban fire losses.

The 2003 Canberra bushfires destroyed more than 500 homes in suburban areas.

In 2021, the Wooroloo fire destroyed 86 homes on Perth’s northeastern fringe.

In 2019, the Gospers Mountain mega-blaze came dangerously close to advancing on Sydney’s urban heart, and was held back by a timely southerly wind change.

These incidents show that major population centres can face serious fire threats, and that near-misses are possible even when disaster is ultimately avoided. From an insurance perspective, repeated close calls and escalating hazard conditions can still influence how risk is assessed and priced.

What this could mean for Australian policyholders

For households, the most immediate concern is affordability and adequacy of cover. If premiums rise, more people may be pushed into insurance stress, or may respond by reducing coverage, increasing excesses, or dropping policies entirely — choices that can widen the protection gap over time.

At the same time, the Los Angeles experience highlights another risk: underinsurance. When cover is capped or when policies exclude key elements of rebuilding, households can find themselves exposed even when they believe they are insured. The practical result is that recovery costs can land on individuals and governments, rather than being spread through insurance pools.

Practical steps Australians can take now

While many drivers of premium increases sit beyond the control of individual consumers, there are still meaningful actions policyholders can take to reduce unpleasant surprises and improve resilience.

Check what your policy covers — and what it excludes. Greater clarification over exclusions was recommended in a recent parliamentary inquiry into the 2022 floods. In the meantime, households can protect themselves by understanding the limits of their own cover.

Review the Product Disclosure Statement (PDS). Policyholders should revisit the terms and conditions that govern their policy, especially ahead of renewal.

Ask questions before renewing. If you are unsure about what a particular policy covers, contact your insurer prior to renewal to clarify inclusions, exclusions, and any changes to terms.

Improve home bushfire resilience where possible. Australians can take steps to make their homes more bushfire resilient, which may also support affordability in some cases.

One initiative highlighted in Australia is a free app launched through a partnership between the Resilient Building Council and the federal government. The app allows homeowners to assess their fire resilience and, by making improvements, potentially earn premium reductions from participating insurers.

A broader reckoning for insurance and risk

The Los Angeles wildfires have intensified scrutiny of how insurance systems respond when climate-driven hazards escalate and losses become more frequent and severe. California’s growing protection gap, insurer withdrawals, and rising reliance on a bare-bones last-resort plan show what can happen when the economics of coverage become strained.

For Australia, the lesson is not that the same outcome is inevitable, but that the conditions that drive insurance stress — rising risk, higher losses, and greater uncertainty — can build over time. The possibility of large-scale urban fire losses, even outside traditional fire seasons, adds to the urgency of preparation.

Above all, Australians need to be aware that under a changing climate, we may be more at risk from fire than we realise, including in major cities. Understanding insurance coverage, reducing vulnerability where possible, and anticipating that global events can affect local premiums are all part of navigating a more uncertain risk landscape.