Weather index insurance: could faster payouts help Australians manage extreme-weather risk?

Australia’s insurance strain is growing as extreme weather changes shape

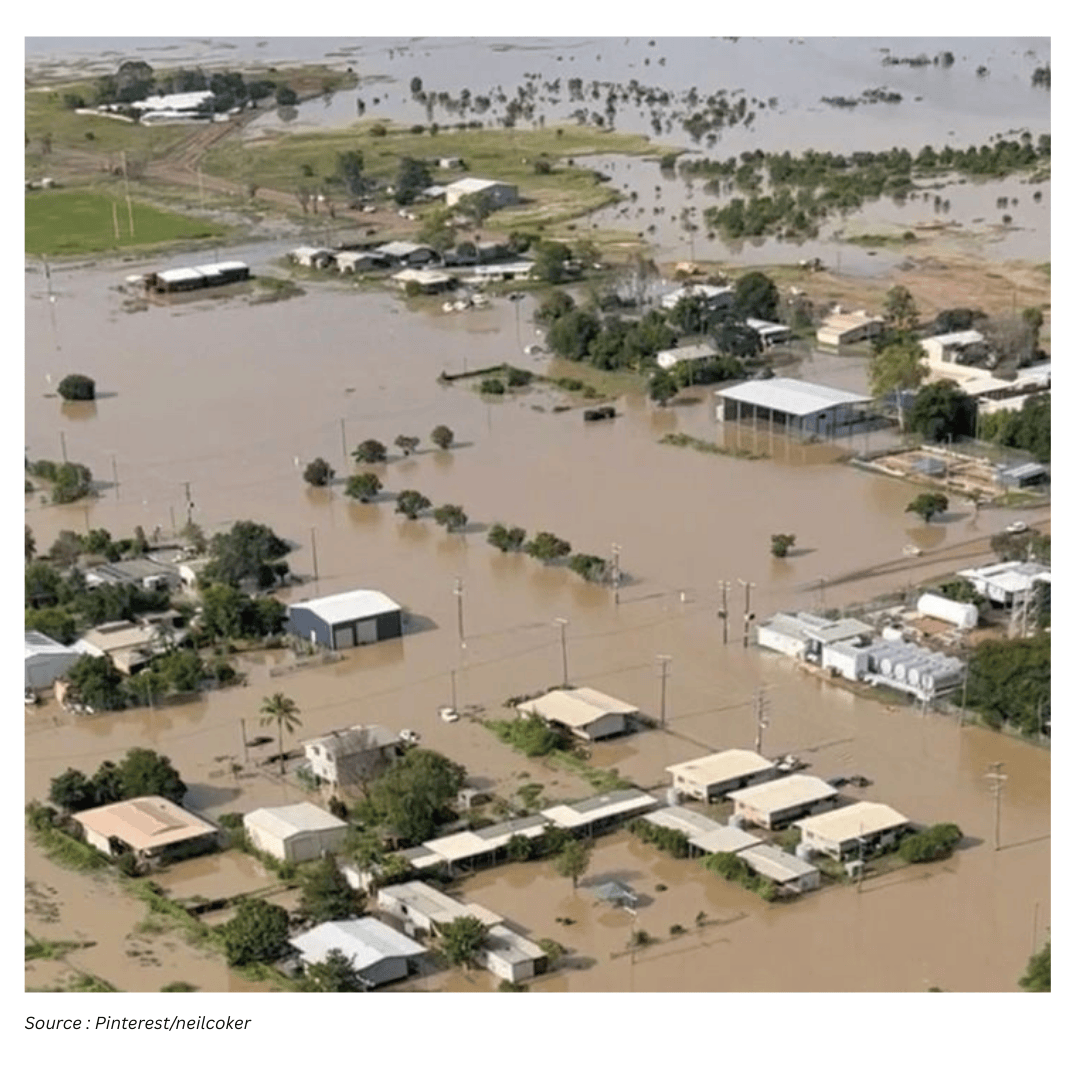

Floods in southeast Australia again exposed a familiar pattern: damage assessments can be slow, claims can take a long time to process, and rising premiums can leave many households and businesses without cover. These pressures are not occurring in isolation. In the insurance industry, there is increasing attention on “secondary perils” — localised, sudden and intense weather events such as thunderstorms, hail, bushfires, drought, flash floods and landslides.

Secondary perils are generally described as less severe than a single, massive catastrophe such as a major earthquake or cyclone. Yet they can happen frequently and still generate substantial damage bills and displace large numbers of people. In 2020, more than 70% of global insured losses from disasters were attributed to secondary perils. Examples noted in Australia include the Black Summer bushfires and a freak hailstorm in Canberra that caused an estimated A$1.65 billion in damage.

Australia is among the countries most exposed to extreme weather associated with climate change. That exposure raises a practical question for consumers, insurers and policymakers: how should financial risk be managed when damaging events are frequent, localised, and sometimes difficult to assess quickly on the ground?

One option increasingly discussed internationally is “weather index insurance” — a form of cover designed to pay out automatically when a predefined weather threshold is met. It is not presented as a cure-all, but it may be one component of a broader rethink about how insurance works under intensifying climate risk.

How traditional claims differ from index-based payouts

Most people are familiar with traditional insurance: a policyholder makes a claim after a loss, and the insurer pays out based on an assessment of damage caused by an event. In major disasters, this process can become slow and complex. Victims may have to compile detailed inventories of what was lost or damaged, and large volumes of claims can overwhelm assessment and processing capacity. The result can be months — or in some cases years — before people receive funds.

Weather index insurance works differently. Instead of paying out after an assessor verifies the extent of damage, the policy pays when an agreed index is reached. The index might be a flood level, a rainfall threshold, or another measurable indicator tied to the risk being insured. For farmers, for example, low rainfall can be used as a trigger for drought-related payments.

The central idea is administrative simplicity and speed. If the index is met, the payout can be rapid and automatic. As soon as the relevant weather event is recorded, the policyholder is paid. This approach is being trialled in multiple countries, most commonly among farmers in remote parts of developing regions.

Why index insurance has been used in remote farming regions

Index insurance has been deployed in places where conventional loss assessment is difficult, slow or costly. After extreme weather, it can be challenging for assessors to travel long distances to remote areas — whether that is the steppes of Mongolia or floodplains of Bangladesh — to inspect farms and verify damage. In these contexts, technologies such as remote sensing and satellites can help insurers determine when extreme weather has occurred.

Because the payout is triggered by the index rather than the observed condition of an individual farm, the payment can occur regardless of whether a crop survives. Proponents argue this can change incentives in a useful way: farmers may be more likely to make decisions aimed at saving a crop, knowing they will still receive the payout if the index threshold is reached. If the crop survives, the farmer can receive both the insurance payout and crop revenue.

Insurers also see index insurance as a way to expand into markets that have been hard to serve with conventional products. The index can be linked to specific crops and their growing conditions, allowing insurers to estimate potential losses and structure policies accordingly.

Potential benefits beyond the payout itself

One argument in favour of weather index insurance is that it can support financial resilience even when the payout is relatively modest. Having insurance can make poorer farmers more creditworthy, potentially improving access to loans. In Ethiopia, a weather index insurance project was found to have benefited farmers in part because speedy payouts reduced the need to sell valuable livestock to cope with disaster impacts. In some cases, farmers were able to reinvest insurance funds into their herds rather than liquidating assets under pressure.

These examples are drawn from agricultural settings, but they illustrate the broader promise of rapid, predictable cash flow after a shock: if funds arrive quickly, households and businesses may be able to avoid the most damaging coping strategies.

What is happening in Australia so far

Research in Australia supports the viability of weather index insurance, and the product has been rolled out to a small number of farmers. However, it is not widely adopted. Australian insurance providers have also offered weather policies overseas. One example cited is CelsiusPro, which has worked with the World Bank and other aid organisations to bring such insurance to communities in the Pacific.

At the same time, the Australian debate about insurance affordability and access has sharpened following recent disasters. When premiums rise and underwriting becomes more restrictive, some people become underinsured or uninsured. Against that backdrop, index-style products are sometimes discussed as a way to reduce administrative delays and make payouts more predictable.

Limits and trade-offs: why index insurance is not a magic bullet

Index insurance comes with significant caveats. A key issue is that the index is typically tied to the growing conditions of a particular plant or crop. That can encourage specialisation, potentially locking farmers into a single crop and exposing them to new risks such as volatile market prices. It can also undermine diversification strategies that are often used to manage uncertainty.

Another challenge is that payouts are not guaranteed in the way many policyholders might expect. If damaging conditions occur but do not meet the index threshold, there may be no payout. An example described from Paraguay involved sesame farmers who experienced flooding followed by drought during an El Niño year. In many areas, conditions fell just short of the index trigger, and farmers did not receive payments despite suffering losses.

Data quality and representativeness can also be a problem. Index insurance depends on measurements — from remote sensing, satellites, weather stations or models — that may not perfectly match what is happening at ground level. Research in sub-Saharan Africa found a sizeable gap between environmental and weather indices measured by remote sensing and the lived experience of policyholders. When the index diverges from reality, the product can feel unfair and may fail to provide the support people believe they have purchased.

Infrastructure, monitoring and the question of who bears the burden

Improving index accuracy and monitoring can require substantial investment by governments and insurers. This may include weather stations, climate models and communications systems. Without reliable infrastructure, it is difficult to design thresholds that are both meaningful and trusted.

In some settings, communities have carried part of the burden of producing good data. In Paraguay, local communities helped maintain meteorological equipment, provided on-the-ground feedback and contributed to crop science, but were often not compensated for this work. This raises questions about the distribution of costs in systems that rely on local participation to function well.

Social impacts: individual policies in collective crises

Weather disasters are often managed collectively, especially in developing countries where community-based responses can be central to recovery. Individual insurance policies may, in some circumstances, reinforce inequalities and erode community-based coping mechanisms. This does not mean insurance is inherently harmful, but it highlights that product design can shape social outcomes — including who benefits first, who is left out, and how recovery resources are distributed.

Uptake has also been limited in many places due to high premiums and low trust among farmers. Trust is particularly important for index insurance because the payout is determined by an abstract measure rather than a visible assessment of damage. If policyholders do not understand or believe in the index, participation may remain low even if the product is technically sound.

Could index insurance work beyond farming — and what remains untested

To date, weather index insurance has not been tested on property insurance in the way it has been used in agriculture. That matters for Australia, where public attention often focuses on household and small business recovery after floods, fires and storms. The slow and difficult experience of waiting for payouts after major floods suggests there is interest in solutions that can deliver funds faster, but translating index-based triggers into property contexts would raise new design questions.

Some research has found merit in exploring weather insurance at a regional or national scale. This points to the possibility that index approaches might not only be individual products, but could be part of larger risk-management arrangements. However, any move in this direction would still need to grapple with data quality, fairness, affordability and trust.

What a “radical rethink” could include

Australia’s high exposure to extreme weather means multiple insurance options may need to be considered, particularly those that are inclusive and do not relegate high-risk communities into a permanent pool of “uninsurables”. Index insurance is presented as one possible piece of the puzzle because it aims to reduce delays and administrative burdens by paying based on measurable triggers.

But the same features that make index insurance attractive — automation and reliance on thresholds — also create risks of mismatch between the index and real losses, and may shift costs onto communities through data collection and monitoring. For these reasons, index products are typically framed as tools to be adopted cautiously, with careful attention to design and governance.

Key points to consider when comparing index insurance with traditional cover

Speed: Index insurance can pay rapidly and automatically once a threshold is met, avoiding long assessment queues.

Assessment burden: Traditional claims often require detailed documentation of losses; index insurance relies on recorded conditions instead.

Basis risk: If the index does not reflect actual on-the-ground damage, policyholders may miss out even after a harmful event.

Data and infrastructure needs: Accurate triggers may require investment in weather stations, models and communications systems.

Incentives and behaviour: In farming contexts, payouts can occur even if a crop survives, potentially encouraging better decision-making under stress.

Equity and trust: Individual policies can interact with community recovery in complex ways; low trust and high premiums can limit participation.

Where this leaves Australia

Secondary perils are becoming a dominant driver of insured losses globally, and Australia’s exposure to extreme weather is high. Recent disasters have highlighted how slow assessments and rising premiums can leave people waiting for support or without insurance altogether. Weather index insurance offers a different mechanism: pay when measurable conditions occur, rather than after damage is individually verified.

International experience suggests the approach can deliver rapid payouts and, in some cases, reduce harmful coping strategies. Yet it also demonstrates real shortcomings — from missed payouts when conditions fall just short of the trigger, to gaps between remote measurements and lived reality, to the need for substantial investment in monitoring systems. As Australia considers how to manage escalating climate-related risk, index insurance may be worth evaluating alongside other reforms, with a clear-eyed view of both its promise and its limits.