NSW floods spotlight a growing crisis: when insurance becomes unaffordable or unavailable

Flood recovery in NSW, and a deeper question about protection

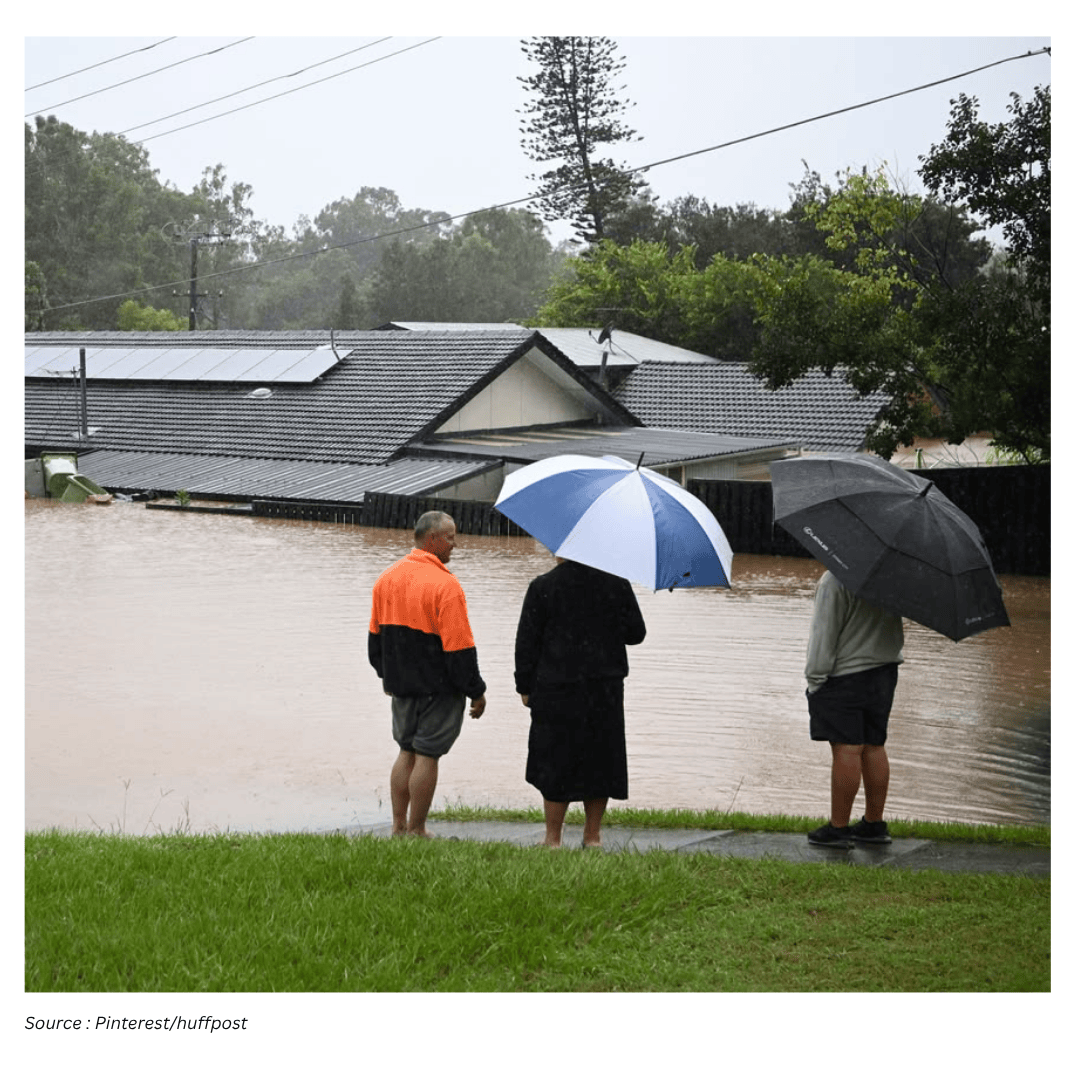

Large parts of New South Wales have again been devastated by floods, triggering a familiar cycle of emergency response, clean-up, and the long, uncertain process of recovery. The scale of damage is significant: it’s estimated 10,000 homes and businesses may have been damaged or destroyed, and the Insurance Council of Australia reports more than 6,000 insurance claims have been received for the Mid North Coast and Hunter region.

Hundreds of families are displaced. With many homes now uninhabitable, they face an uncertain future shaped not only by the physical damage, but also by whether they can access insurance cover that is affordable, comprehensive and reliable when it is needed most.

As the mop-up begins, stories are emerging of households and businesses not covered by insurance at all. Some residents say insurers were asking up to A$30,000 annually for cover. Others are underinsured, where insurance payouts do not meet the full costs of rebuild, repair and replacement. The Insurance Council of Australia has declared the event an “insurance catastrophe”.

These details matter because they point to a broader issue: the immediate disaster is the flood, but the longer-running crisis is the erosion of insurance affordability and availability for households, businesses and communities.

From isolated hardship to an unfolding pattern

It is tempting to frame insurance stress as a temporary consequence of a single extreme event. Yet the experience in NSW reflects a wider trend. In 2024, there were around 60 natural disaster events that each exceeded A$1.5 billion in economic losses. Total losses worldwide reached A$650 billion.

In a country described as one of the most disaster-prone in the Western world, these pressures prompt an uncomfortable question: is Australia becoming an early indicator of a wider breakdown in how private insurance can function in the face of escalating disasters and a changing climate?

That concern is not new. In 1992, sociologist Ulrich Beck argued unpredictable global risks, such as climate change, would bring an end to the private insurance market, with profound effects on the modern world. Today, the prospect of an “uninsurable future” can evoke dramatic imagery—crumbling buildings, deteriorating streetscapes, and people trying to get by amid ruins.

But the more immediate reality is less cinematic and more practical: in places including central NSW, the problem is not only about what might happen years from now. Many individuals and communities are already living with an unfolding collapse of insurance affordability and availability. The consequences can be dire, especially for those already struggling to make ends meet.

Political pressure focuses on insurers, but the system is larger

After major disasters, public attention often turns to insurers: how quickly claims are processed, how much is paid, and whether customers are treated fairly. Speaking on ABC radio on Thursday morning, NSW Premier Chris Minns said he would be “putting the heat” on insurance companies, adding that “Everyone’s going to have to do their part […] and that means insurance companies will have to step up and pay out claims quickly.”

In the lead-up to the federal election, both major parties signalled they believed insurers were “ripping off” Australians. The Coalition proposed new emergency divestiture powers that would allow the government to break up major insurers in the case of market failure.

However, the pricing and coverage decisions that shape household premiums and policy terms are not only determined by local insurers. They are also heavily influenced by global “reinsurers”—companies that provide insurance coverage for insurers themselves, helping cover the cost of paying out claims after major disasters.

This matters because reinsurance is concentrated. Just ten multi-billion dollar companies control 70% of the reinsurance market. In practice, that means the affordability and availability of cover in disaster-prone regions can be tied to decisions and risk models that sit well beyond a single state, a single insurer, or even a single national market.

When premiums rise and cover retreats

One of the most damaging features of the current trajectory is how predictable it has become. After each major disaster event comes a rise in insurance costs and a withdrawal of insurance coverage. For households, that can translate into painful trade-offs: pay more for the same cover, accept higher excesses, accept narrower coverage, or drop insurance entirely.

The impacts are not limited to one product line. In places like Australia, the increasing cost of insurance cuts across all types, with the largest rises coming in home, vehicle, and employers’ liability insurance.

For people already under financial pressure, these changes can be destabilising. Underinsurance—where the policy exists but does not cover the full costs of rebuild, repair and replacement—can leave families and small businesses facing a shortfall at the worst possible time. And for those priced out completely, the absence of cover can turn a damaging event into a life-changing one.

Industry growth can coexist with household stress

It is easy to assume that if insurance becomes unaffordable for many customers, insurers must be struggling too. Yet the sector’s financial performance does not necessarily align with household experience.

Many insurers are reporting healthy profits. Globally, the sector is experiencing “exceptionally strong growth”. Over the three years to 2024, revenue from premiums in the insurance sector increased by over 21% globally—a “whopping” rise, according to the finance corporation Allianz.

From a consumer perspective, this creates a tension: the industry can expand and profit even while more people find cover too expensive or too limited to be meaningful. The sector may continue to grow—and profit—until it no longer can due to climate change and other pressures. But the most immediate concern is not a future crash of insurers. It is the real-time collapse of insurance for households, businesses and communities.

Resilience shifts to households and communities

As this collapse of insurance unfolds, it is largely left to households and communities to take action and build resilience. In the wake of repeated disasters, that can mean people improvising solutions in the absence of stable housing and financial support.

Examples cited include squatters taking possession of flood-damaged vacant homes in Lismore and, when combined with the housing crisis, the growth in informal housing and settlements on the fringes of major population centres.

These responses are described as desperate. They are also presented as realistic, given the view that governments and insurers are failing to reverse the trending collapse.

Policy proposals: mitigation funding and retrofits

Insurers, led by the Insurance Council of Australia, are pushing for a Flood Defence Fund and retrofitting homes for disaster resilience, paid for by governments and households.

On the surface, these ideas can sound straightforward: reduce risk, reduce damage, and insurance becomes more viable. Yet the critique raised is that such proposals can draw attention away from other issues—namely, an industry that is thriving, and the need for regulations and policies aimed at making insurance more affordable and effective for ordinary people.

This is an important distinction. Disaster mitigation and resilience upgrades may be part of the answer, but the question remains: who pays, who benefits, and whether these measures are sufficient to prevent cover from continuing to retreat in high-risk areas.

Why “insurability” is becoming a community issue

Insurance is often treated as an individual purchase: a household chooses a policy, pays a premium, and manages its own risk. But repeated disasters can turn insurance into a community-level problem. When large numbers of people cannot obtain affordable cover, the impacts ripple outward.

Displacement rises when homes cannot be repaired quickly or rebuilt. Local economies suffer when businesses cannot reopen or replace equipment. Inequality can deepen if those with resources can insure and rebuild, while those without resources are left exposed or forced into precarious housing.

In this sense, “insurability” is not only about whether a company will offer a policy. It becomes a question of how communities remain liveable and economically functional when protection against disaster is no longer broadly accessible.

What government intervention could look like

To avoid being a “canary in the coalmine”, the argument presented is that Australia urgently needs government intervention in the insurance industry—an industry described as very resistant to such intervention.

One option raised is an equitable and affordable public insurance scheme, designed to ensure everyone is adequately covered when disaster strikes. Such a scheme is framed as a way to address the widening gap between rising risk and shrinking access to meaningful cover.

At the same time, the challenge is not only technical or financial. As more Australians lose the ability to insure themselves, governments are urged to address growing structural inequality that is undermining social cohesion and the capacity for collective resilience.

Key takeaways from the NSW floods debate

NSW’s latest floods have damaged or destroyed an estimated 10,000 homes and businesses, with more than 6,000 claims reported for the Mid North Coast and Hunter region.

Some households and businesses report being uninsured due to cost, including annual premium quotes as high as A$30,000, while others are underinsured and face major rebuilding shortfalls.

Globally, 2024 saw around 60 natural disaster events exceeding A$1.5 billion in economic losses, with total worldwide losses of A$650 billion—context that reinforces the scale of the challenge.

Political pressure often targets insurers, but pricing and coverage are influenced by global reinsurers, with ten companies controlling 70% of the reinsurance market.

Insurance costs are rising across multiple categories, with the largest increases noted in home, vehicle, and employers’ liability insurance.

Despite affordability stress for consumers, the global insurance sector is described as experiencing exceptionally strong growth, with premium revenue up more than 21% over three years to 2024.

Proposals such as a Flood Defence Fund and home retrofits are being advanced, but the debate also centres on regulation and policy focused on affordability and effectiveness for ordinary people.

A public insurance scheme is proposed as one potential form of intervention, alongside action to address structural inequality that weakens collective resilience.

A crisis measured in premiums, coverage gaps and displacement

The NSW floods have once again made visible what can otherwise remain hidden in policy documents and renewal notices: when insurance becomes too expensive or too limited, the burden of disaster recovery shifts sharply onto individuals and communities. That shift can be felt in the immediate aftermath—through displacement and uncertainty—but also in the longer term, as people make housing and livelihood decisions in an environment where protection is no longer assured.

In this framing, the central issue is not whether insurers will continue to exist next year. It is whether households, businesses and communities can access insurance that is affordable and effective as disasters escalate, and whether public policy is prepared to respond to an unfolding collapse of insurability before it becomes entrenched as a new normal.